Click free trial.Middle finger data product

In 2023, "the relationship between supply and demand in the real estate market has undergone major changes", and the property market has been adjusted. Government departments at all levels have frequently optimized the property market policies to promote the smooth operation of the real estate market. The policy environment is close to the most relaxed stage in 2014, but factors such as weak residents’ income expectations and falling house prices are still restricting the pace of market repair. The adjustment situation of the new house market has not changed, and the effect of the core city policies is insufficient. The second-hand housing market in key cities performs better than the new housing market under the condition of price-for-volume exchange.

Looking forward to 2024, the recovery of the real estate market still depends on whether the buyers’ expectations can be repaired, and there is still room for policy development at both ends of supply and demand. The "three major projects" will be the main direction of policy development, which is expected to play an important role in stabilizing investment next year, and will also play a positive role in sales recovery and stabilizing expectations. On the whole, the new home sales market is still facing adjustment pressure in 2024. If the economy continues to recover and the willingness to buy homes improves, the reconstruction of superimposed villages in the city will advance as scheduled, and the sales scale may increase slightly. Under the influence of the slow repair of the sales market, the downward trend of new construction and investment in the country may be difficult to change.

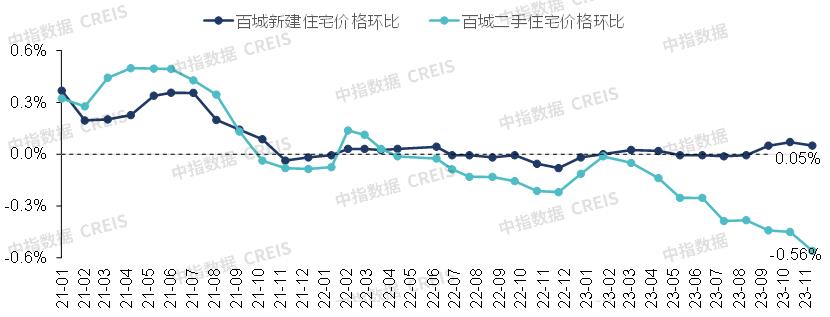

(1) house price:From January to November, the price of new residential buildings in Baicheng increased by 0.16%, mainly due to factors such as policy control and the entry of some high-quality improved properties into the market, and the price of new houses rose structurally. From January to November, the price of second-hand residential buildings in Baicheng dropped by 3.00%, which was 2.45 percentage points higher than the same period of last year. The trend of house prices continued to be sluggish. By November, it had fallen for 19 consecutive months, and the number of cities that fell for 6 consecutive months exceeded 90.

(2) Market supply and demand:From January to November, the sales area of new commercial residential buildings in key 100 cities decreased by about 5% year-on-year, and the sales scale of second-hand houses in key 15 cities increased by 35% year-on-year from January to October. Throughout the year, driven by the concentrated release of demand after the epidemic, the market warmed up obviously in the first quarter, the volume and price dropped in the middle of the year, and the market performance was sluggish. At the end of August, the central government and governments at all levels stepped up their efforts to support the bottom, and the year-on-year decline in new home sales from September to October narrowed, but the policy effect was not sustained enough, and the market still faced downward pressure at the end of the year. The approved listing area of 50 commercial houses representing cities decreased by more than 10% year-on-year, the saleable area declined slightly but remained at a high level, and the short-term inventory clearing cycle was extended to 19.5 months.

(3) Demand structure:Since 2023, the demand for improved housing remains the key support of the new housing market. The average, median and price thresholds of most cities in 30 representative cities are higher than the same period of last year. In terms of area, 90-120 square meters of products still occupy the mainstream position in the market. With the gradual cancellation or optimization of property market regulation policies in cities, the demand for re-reform and high-end improvement has been released, and the improvement of the market has shown some resilience.

(4) Land market:From January to November, the launch and transaction area of residential land in 300 cities nationwide decreased by 21.5% and 28.0% respectively compared with the same period of last year. Only some cities or individual plots were hot, and the overall downturn remained unchanged.Focus on 22 citiesThe transaction volume of high-quality land plots has increased, and the central state-owned enterprises are the main land acquisition, accounting for 50% of the land acquisition, and the investment of private enterprises is still insufficient. By the end of November, except for Beijing, Shanghai and Shenzhen, most cities have cancelled the maximum land price, but only a few high-quality plots in core cities have been auctioned at a high premium, and the overall heat is still low.

(5) Policy prospect:Demand side, the futureJinghuIt is expected to reduce the down payment ratio of the second suite, lower the mortgage interest rate, optimize the identification standard of general housing, and reduce transaction taxes and fees. In addition, it is also possible for first-tier cities to optimize suburban purchase restrictions according to the policy of different regions;Core second-tier citiesIt is expected that more cities will completely cancel the purchase restriction 3; More low-level cities may promote the release of housing demand by issuing housing subsidies.Supply endThe enterprise-side financial support policy is expected to continue to be implemented in detail, and the corporate financing environment is expected to be improved; The funds and supporting measures of "Baojiaolou" may be further followed up, and the rules of local auctions are expected to continue to be relaxed; In addition, policies related to the construction of the "three major projects" are expected to accelerate.

(6) Market prospect:

According to the "dynamic model of the long-term development of China real estate industry", in 2024, the national real estate market will show the characteristics of "downward pressure on sales scale, new construction area and development investment may continue to fall". Under neutral circumstances, it is estimated that the national commercial housing sales area will decrease by 4.9% year-on-year. Under optimistic circumstances, in 2024, the macro-economy will continue to recover, the residents’ willingness to buy homes will improve, and the reconstruction of superimposed villages in the city will be promoted as scheduled, and the national commercial housing sales area may achieve a small increase. However, new construction and investment are affected by many unfavorable factors, or the downward trend will continue. Under neutral circumstances, the newly started area in 2024 decreased by about 10% year-on-year, and the newly started scale was less than 900 million square meters; Investment in real estate development decreased by 6.1% year-on-year.

Summary of China real estate market situation in 2023

The entry of improved properties into the market led to a slight increase of 0.16% in the price of new houses in Baicheng from January to November; In the first 11 months, the price of second-hand houses fell by 3%, maintaining the decline throughout the year, with prices falling in over 90% of cities.

Figure: The price changes of newly-built and second-hand houses in Baicheng since 2021.

Market monitoring: https://www.cih-index.com/

In terms of new residential buildings, the price of new residential buildings in Baicheng increased by 0.16% from January to November 2023. Driven by policy control and some quality improvement projects entering the market, the price of new residential buildings rose slightly month-on-month since September.

Specifically, at the beginning of the year, driven by the favorable policies of the property market, such as the comprehensive lifting of epidemic prevention and control, the reduction of down payment and interest rate, the backlog of housing demand was actively released and market confidence was temporarily restored; With the release of the backlog of demand, the activity of the new housing market declined in the middle of the year, and house prices also re-entered the downward channel; In August, many ministries and commissions took measures to optimize the property market. Later, housing enterprises also actively pushed goods for preparing for the "Golden September and Silver 10". Driven by some high-quality improvement projects entering the market, the price of new houses in Baicheng increased slightly from September to November. In November alone, the average price of new residential buildings in Baicheng was 16,203 yuan/square meter, up 0.05% from the previous month.

In terms of second-hand housing, from January to November, 2023, the price of second-hand housing in Baicheng dropped by 3.00%. After the decline of second-hand housing prices narrowed for a short time at the beginning of the year, house prices entered an accelerated downward channel in the middle of the year.

Specifically, at the beginning of 2023, due to the release of the backlog of home purchase demand, the transaction of second-hand houses maintained a high activity, which led to a short-term narrowing of the decline in the price of second-hand houses in Baicheng; In the middle of the year, the downward pressure on the market increased, and the decline in house prices expanded. After the implementation of the policy of "recognizing houses but refusing loans" in September, the demand for changing houses pushed up the listing of second-hand houses in key cities, and the downward trend of house prices was more obvious. In November, the average price of second-hand residential buildings in Baicheng was 15,400 yuan/square meter, down 0.56% from the previous month, which has been falling for 19 consecutive months.

Figure: Since 2021, the prices of newly-built and second-hand houses in 100 cities have fallen month-on-month, and the number of cities has changed.

Market monitoring: https://www.cih-index.com/

In terms of the number of rising and falling cities, from January to November, 2023, the cumulative number of cities where the price of newly-built housing fell was 64, and the number of cities that fell month-on-month basically remained in the range of 40-50. From January to November, the number of cities with a cumulative decline in the price of second-hand housing was 97, while the number of cities with a month-on-month decline in price showed a trend of first decline and then increase. In March, the number of cities with second-hand housing prices dropped to 68, and since April, the number of cities with second-hand housing prices dropped continuously. In November, the number of cities with second-hand housing prices in 100 cities dropped to 99, surpassing 90 cities for six consecutive months, and the price of second-hand housing showed a general downward trend.

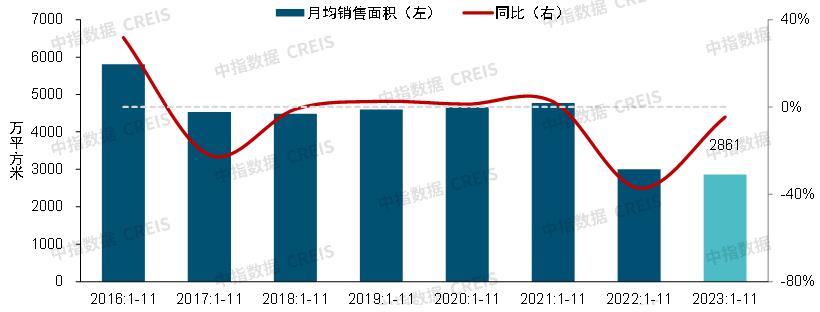

From January to November, the transaction area of new houses in key 100 cities decreased by about 5% year-on-year, and the adjustment trend may continue at the end of the year.

National:

According to the data of the National Bureau of Statistics, from January to October 2023, the sales area of commercial housing nationwide was 930 million square meters, down 7.8% year-on-year, and the sales of commercial housing was 9.7 trillion yuan, down 4.9% year-on-year, of which the sales area of commercial housing decreased 6.8% year-on-year and the sales decreased 3.7% year-on-year. From January to October, the sales of existing houses reached 200 million square meters, up 15.6% year-on-year, which was obviously better than that of forward houses. In terms of proportion, the sales area of existing houses accounted for 21.5% of the total sales area, up 4.2 percentage points from the end of 2022.

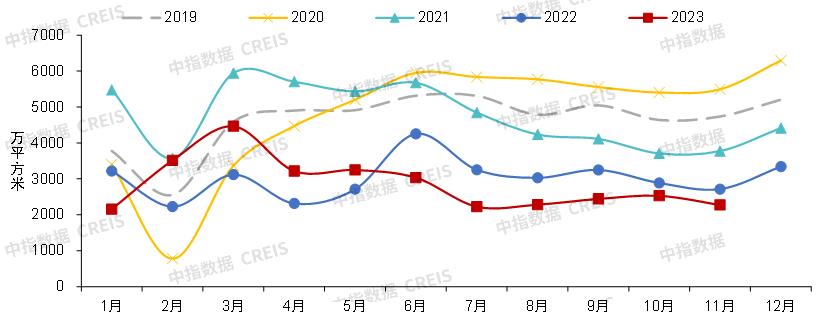

Figure: Average monthly sales area and year-on-year trend of newly-built commercial housing in 100 representative cities from 2016 to 2023 from January to November.

Figure: Monthly sales area trend of new commercial housing in 100 representative cities since 2019

Market monitoring: https://www.cih-index.com/

Key 100 cities:

From January to November 2023, the transaction area of new commercial housing in key 100 cities decreased by about 5% year-on-year, and the absolute scale was the lowest in the same period since 2016.

According to preliminary statistics, from January to November 2023, the average monthly sales area of new commercial housing in key 100 cities was about 28.61 million square meters, down 4.6% year-on-year. Specifically, driven by the concentrated release of demand after the epidemic, the market warmed up significantly at the beginning of the year, with a low cardinal utility. The sales area increased by 23% year-on-year from January to April, and the volume and price fell in the middle of the year, resulting in a sluggish market performance. Since the end of August, many core cities have successively implemented the policy of "recognizing houses but not loans" and optimizing the policies of restricting purchases and sales. The policy environment is close to the most relaxed stage in 2014, but residents’ expectations have not improved significantly, and the policy-driven effect is relatively good. In November, the sentiment of home buyers continued to weaken, and the sales area of key cities decreased by about 8% month-on-month and 14% year-on-year. At the end of the year, the market still faced downward pressure.

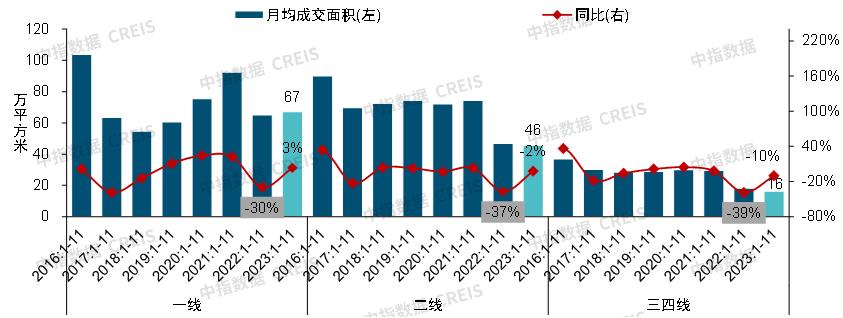

Figure: From 2016 to 2023, the average monthly transaction area and year-on-year trend of urban commercial housing represented by each echelon from January to November.

Market monitoring: https://www.cih-index.com/

From January to November, from the perspective of different echelon cities, among the representative cities, the cumulative sales area of new commercial housing in first-tier cities increased year-on-year, while the second-tier, third-and fourth-tier cities all decreased year-on-year.

According to preliminary statistics, from January to November 2023, the average monthly transaction volume of new commercial housing in first-tier cities was 670,000 square meters, up about 3% year-on-year. Among them, under the low base, the cumulative sales area of Shanghai and Guangzhou increased by 10.9% and 1.3% respectively, while the cumulative sales area of Beijing and Shenzhen decreased by 11.1%.

The second line represents the city.

The average monthly transaction volume of commercial housing was 460,000 square meters, down 2.3% year-on-year, and the transaction scale was still at the lowest level in the same period since 2016. Driven by the influence of low base and the centralized filing of some large-scale cities, the year-on-year decline in sales area of second-tier representative cities in October was significantly narrowed, but in November, the market activity of many cities weakened and the policy effect was insufficient.

The third and fourth lines represent cities.

After entering the fourth quarter, the cumulative year-on-year decline continued to expand, and most cities were under great market adjustment pressure. Some cities, such as Huizhou and Zhenjiang, saw a year-on-year increase in cumulative sales area at a low base, but the absolute scale was still at a low level in the same period in recent years, and the market sentiment continued to be sluggish.

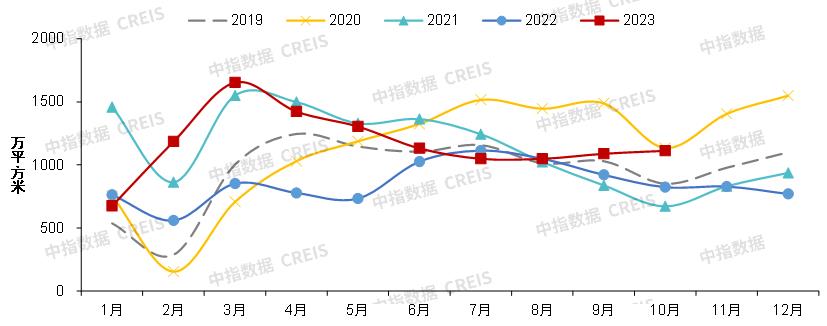

Figure: Trend of monthly transaction area of second-hand residential buildings in 15 representative cities since 2019

Figure: The trend of the number of second-hand residential transactions in Zhou Du in 11 representative cities since 2022.

Market monitoring: https://www.cih-index.com/

The second-hand housing market maintained a certain activity, and the sales area increased year-on-year under the effective policies and low base.

From January to October 2023, the cumulative transaction area of second-hand houses in 15 representative cities was about 116.7 million square meters, up 35.4% year-on-year, and the absolute scale was at a high level since 2019, second only to the same period in 2021. In the first half of the year, the pace of the second-hand housing market was basically the same as that of the new housing market. However, due to the backlog of demand at the end of last year and the buyers’ worries about the delivery of faster housing, the sales of second-hand housing in key cities increased significantly at the beginning of the year. From January to May, the sales increased by nearly 70% year-on-year, and the same market enthusiasm declined in the middle of the year. From September to October, driven by policy optimization and low base, the second-hand housing market performed relatively well, and continued to grow year-on-year. In October In November, the performance of the second-hand housing market was relatively stable, maintaining growth year-on-year at a low base. In the first four weeks of November, the average number of transactions in key cities increased by 17.0% compared with that in October, and increased by 24.1% compared with the same period of last year. The second-hand housing market maintained a certain activity.

The total price of new houses in several cities has increased, and the proportion of middle and high total prices has increased. The demand for improved housing is still an important support.

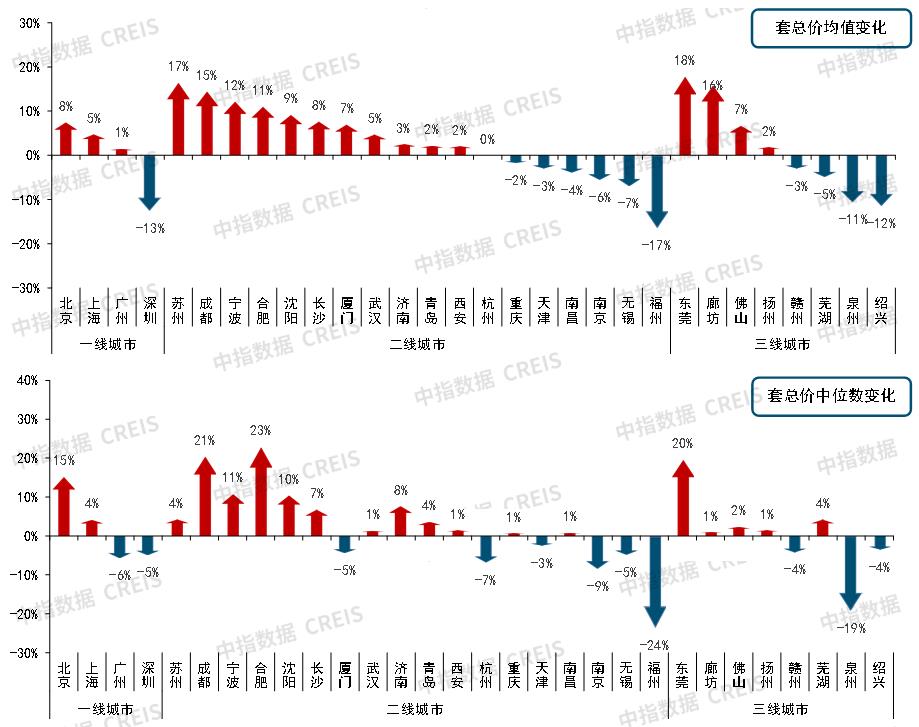

Figure: Year-on-year change chart of the average and median total price of 30 representative cities from January to October 2023.

Market monitoring: https://www.cih-index.com/

From January to October, 2023, the average and median price of 16 apartments in 30 representative cities increased year-on-year, while the average and median price of 8 apartments decreased, especially in Beijing, Hefei, Chengdu and Dongguan.

The main reasons are as follows: First, the clearing of the real estate industry continues, the risks of individual housing enterprises are exposed, consumers’ confidence in buying houses is insufficient, and the wait-and-see mood of those who just need to buy houses has not improved significantly. Improving products to enter the market has driven the release of improved housing demand, which has led to an increase in the total package price. Second, during the year, policies such as "recognizing the house and not recognizing the loan" for the first suite and lowering the interest rate of the second set of commercial loans continued to land, which further promoted the release of demand for improved housing.

In several key cities, the number of transactions in the middle and high total price segments increased year-on-year, and the proportion increased, while the number of transactions in the low total price segment decreased year-on-year.

In Beijing, Shanghai, Chengdu, Changsha and other cities, the proportion of transactions in the middle and high total price segments continued to increase. Among them, the number of transactions in the total price segment of 5-10 million in Beijing from January to October increased by 29.3% year-on-year, accounting for an increase of 8.7 percentage points, while the number of transactions in products below 5 million decreased by 16.2% year-on-year and the proportion decreased by 8.8 percentage points. The number of projects with a total price of 2.5-5 million and more than 5 million in Chengdu increased by over 30% year-on-year at a low base, accounting for 8.1 and 2.1 percentage points respectively.

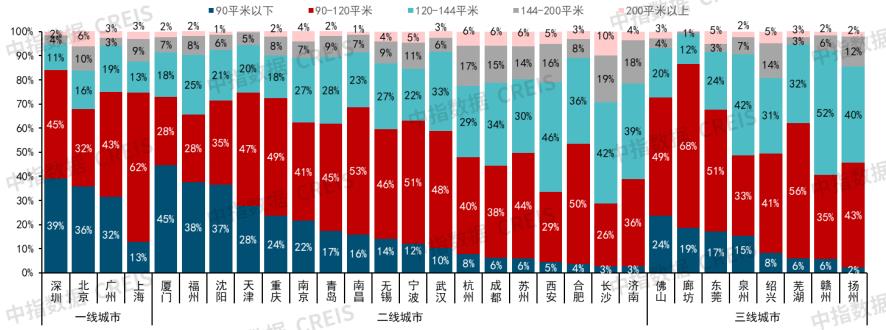

Figure: Proportion of residential sales in 30 representative cities from January to October 2023.

Market monitoring: https://www.cih-index.com/

Judging from the transaction area segment,

90-120 square meters of products are still the main demand in the new housing market. Compared with the same period of last year, among the 30 representative cities, the proportion of new houses with an area of over 120 square meters in 16 cities has increased, and the proportion of new houses with an area of 120-144 square meters in 18 cities has increased, especially in core second-tier cities such as Hefei, Xi ‘an and Chengdu. In addition, as more and more new housing products are positioned to meet the demand for improved housing, the proportion of products with an area of less than 90 square meters in half of the 30 representative cities has declined.

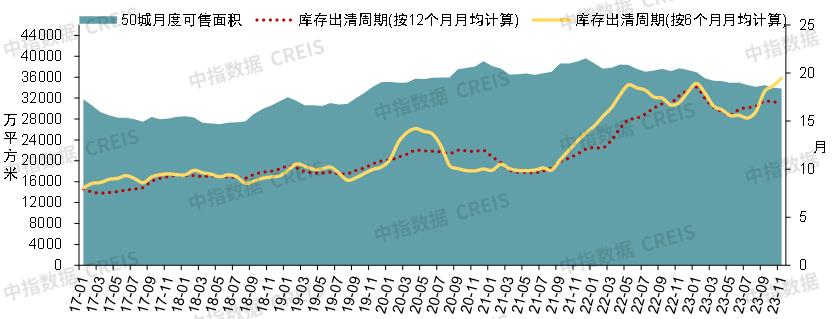

Both the supply and demand sides of the market weakened, the saleable area fell but remained at a high level, and the clearing cycle was extended to 19.5 months.

Nationwide: the year-on-year decline in newly started housing area is still relatively large, and the construction area continues to decline year-on-year.

From January to October, 2023, the newly started housing area in China was 790 million square meters, down 23.2% year-on-year, and the decline rate was 0.2 percentage point narrower than that in January-September. The national housing construction area was 8.23 billion square meters, a year-on-year decrease of 7.3%. The completed area of housing in China was 550 million square meters, up 19.0% year-on-year. In 2023, the work of "guaranteeing the delivery of the building" continued to advance, and the completed area in a single month kept growing year-on-year.

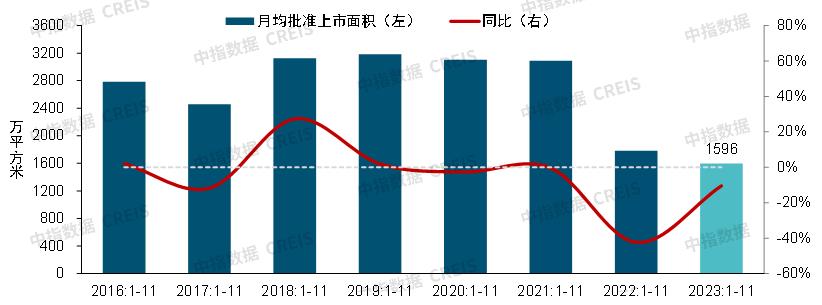

Figure: Trend of average approved listing area of commercial housing in 50 representative cities from January to November from 2016 to 2023.

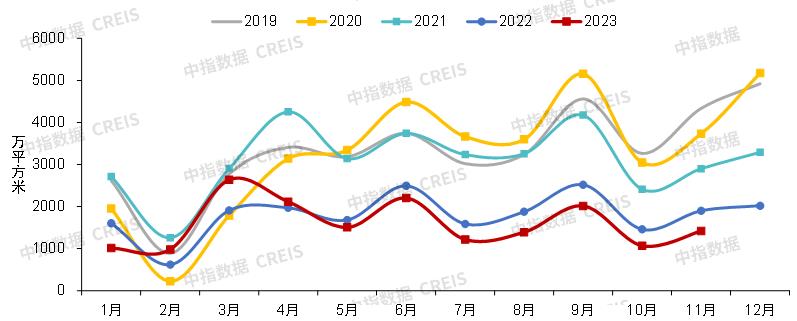

Figure: Trend of approved listing area of commercial housing in 50 representative cities since 2019

Market monitoring: https://www.cih-index.com/

Key cities: the supply capacity and willingness of housing enterprises are insufficient, and the approved listing area of commercial housing in 50 representative cities decreased by over 10% year-on-year.

According to preliminary statistics, from January to November 2023, the average approved listing area of commercial housing in 50 representative cities was close to 16 million square meters, down by about 10% year-on-year (the sales area of the same caliber decreased by about 4% year-on-year), and the overall performance of the supply side was weak. Specifically, in the first half of the year, the supply scale increased slightly by about 2% year-on-year at a low base; However, after entering the third quarter, due to the sluggish sales and limited land acquisition in the early stage, the enthusiasm and ability of real estate enterprises to promote sales are weak, and the approved listing area of new houses has dropped significantly year-on-year. Since July, the monthly approved listing area has dropped by more than 20% year-on-year. In November, under the goal of sprinting the annual performance, housing enterprises accelerated the pace of project supply, and the approved listing area of 50 representative cities increased from the previous month, with an increase of over 30% from the previous month, but the year-on-year decline still exceeded 20%.

In terms of the ratio of sales to supply, under the background of weak supply and demand, the overall performance of the key 50 cities is less than demand.

According to preliminary statistics, from January to November 2023, the average monthly new supply of commercial housing in 50 representative cities was close to 16 million square meters, and the average monthly transaction area was 19.65 million square meters in the same period. The ratio of sales to supply was 1.23, which was higher than the same period last year. Among them, it was 1.47 in the first quarter, 1.14 in the second quarter, and 1.04 in the third quarter. In November, the supply rebounded but remained weak, and the ratio of sales to supply was 1.16, and the situation of supply less than demand remained unchanged.

Figure: saleable area and clearing cycle of commercial housing in 50 representative cities since 2017

Market monitoring: https://www.cih-index.com/

Affected by the overall weakness of the supply side,

By the end of November, the saleable area of commercial housing in 50 representative cities was about 340 million square meters, down 9.4% from the end of 2022, but the scale was still at a high level in recent years. In terms of clearing cycle, as of the end of November 2023, according to the average monthly sales area of nearly six months, the short-term inventory clearing cycle of key 50 cities was 19.5 months, 1.4 months longer than that of the end of 2022, of which the short-term inventory clearing cycle of the third and fourth lines represented 28.1 months, and the short-term inventory clearing pressure was high.

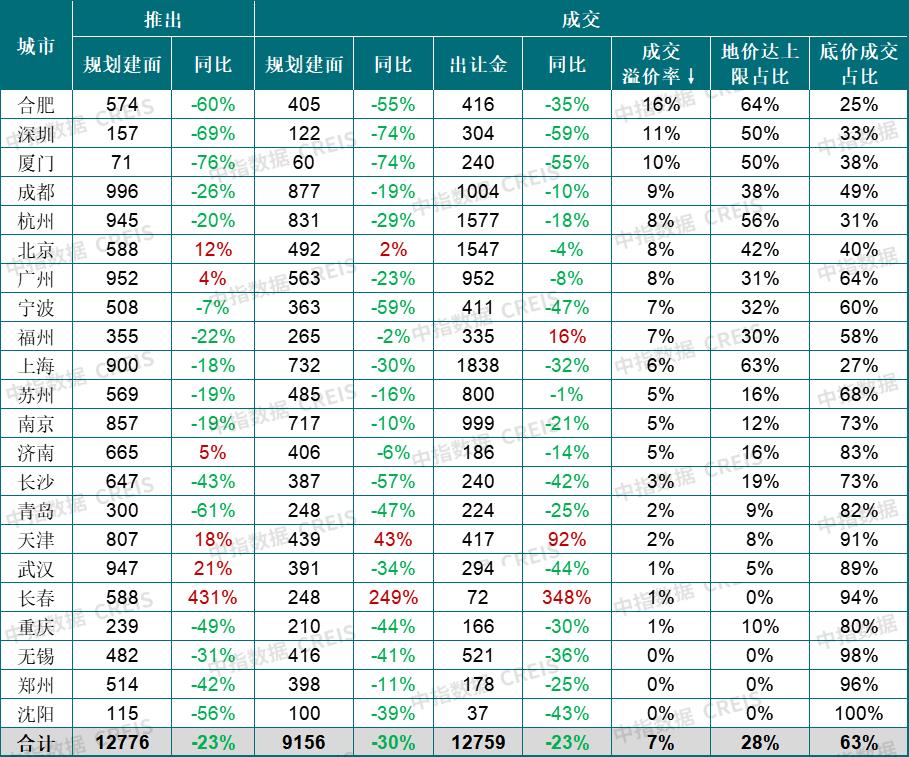

The transaction area of residential land in 300 cities decreased by nearly 30% year-on-year. The central state-owned enterprises are still the main land buyers. At the end of the year, the land price ceiling was abolished in many places, and the differentiation of land auctions intensified.

According to preliminary statistics, from January to November, 2023, the scale of supply and demand of residential land in 300 cities nationwide decreased by more than 20% year-on-year, of which 570 million square meters were launched, down 21.5% year-on-year; The turnover was 340 million square meters, down 28.0% year-on-year, and the absolute scale was the lowest in the same period of the past decade. The overall downturn of Tupai has not changed. In order to improve the willingness of housing enterprises to participate in the auction, local governments have continuously adjusted the land supply structure, driving the average transaction floor price to increase by 8.8% year-on-year.

In terms of the withdrawal of cards from the auction, the number of cases and the rate of withdrawal of cards from the auction of residential land in China continued to decline.

Investigate its reason, on the one hand.

This year, many local governments issued a list of land to be sold for housing enterprises to make decisions in advance before land transfer, reducing the possibility of land auction; On the other hand, it is to continue to increase the intensity of core areas or high-quality plots and improve the certainty of the project. According to preliminary statistics, from January to November, 2023, there were 2,961 plots of land for auction in China, and 454 plots were withdrawn, with a withdrawal rate of 22.9%, which was 6.9 percentage points lower than that of the same period last year, but the overall withdrawal rate of auction was still high.

Table: Supply and demand of urban residential land in each echelon from January to November, 2023

Market monitoring: https://www.cih-index.com/

The scale of launch and transaction in all cities decreased year-on-year, and the launch area of third-and fourth-tier cities decreased significantly. In terms of launch,

According to preliminary statistics, from January to November 2023, the area of residential land in second-tier, third-tier and fourth-tier cities decreased by about 20% year-on-year, while the decline in first-tier cities was relatively small. In terms of transaction, under the influence of factors such as the cautious investment of housing enterprises, the transaction area of each city decreased by nearly 30% year-on-year, and the land transfer fee also decreased to varying degrees.

In terms of floor price, affected by the increase in the proportion of high-quality land transactions in the core area, all cities in each line showed different degrees of increase.first-tier cityThe overall mood of land auction is stable, with the average floor price rising by 8.6%. Among them, many plots in Beijing and Shanghai have been auctioned to the upper limit of land price this year, while the competition of housing enterprises in Guangzhou and Shenzhen is relatively weak, and some plots in Guangzhou have even been auctioned.second-tier cityThis year, high-quality land plots have been continuously launched, and the average transaction floor price has increased by 10.3% as a whole. Since October, plots in Jinan, Hefei, Chengdu and Fuzhou have successively bid for higher premium rates.Third and fourth tier citiesIn China, the land market in most cities is in a downturn, and the average transaction floor price has increased by 6.3% in some cities, such as Dongguan, Foshan, Changzhou and Yancheng.

Table: Transaction of two concentrated residential land in the city from January to November 22, 2023 (city level, 10,000 square meters, 100 million yuan)

Market monitoring: https://www.cih-index.com/

In terms of soil beat heat,In 2023, under the influence of the slow repair of the sales end of new houses, the land acquisition strength and strategy of housing enterprises have not changed.Beijing, Shanghai, HangzhouIt is still the focus of land acquisition by housing enterprises, and many plots have peaked. The land price in Hangzhou and Shanghai accounts for about 60% of the upper limit;Chengdu, Hefei, Xiamen, Guangzhou, NingboIn other places, housing enterprises focus on high-quality sectors, and these plots are generally fiercely competitive, driving the overall urban plots to reach the upper limit, accounting for over 30%.Tianjin, Suzhou, Nanjing, Qingdao and ChongqingIn other places, the adjustment pressure of the new housing sales market in most areas is relatively high, and only a few plots of real estate enterprises are highly concerned.Wuxi, Zhengzhou, Shenyang, ChangchunIn other places, the short-term land market downturn has not changed, and the land sold is sold at the reserve price.

In addition, according to media reports, at the end of September, the Ministry of Natural Resources has issued documents to the natural resources authorities of various provinces and cities, including suggestions to cancel the land price restrictions in land auctions. As of the end of November, 18 of the 22 cities have actually implemented the "cancellation of land price limit", but Beishangshen has not been adjusted, and the upper limit of Ningbo premium rate has been raised from 15% to 30%.Judging from the performance of soil auction, the cancellation of price limit has driven the soil auction of a small number of high-quality plots in core cities to heat up.On October 30,JinanOf the 10 land transactions, 3 have a premium rate of over 50%. On November 15th,ChengduAmong the 7 plots sold, 1 plot had a premium rate of 30%, 1 plot had a premium rate of 17%, and the rest were sold at the reserve price. On the 30th, among the five plots sold in Chengdu, the premium rate of Luhu plot in Tianfu New District reached 61%, which was acquired by Rundafeng Real Estate, and the rest plots were sold at the reserve price.

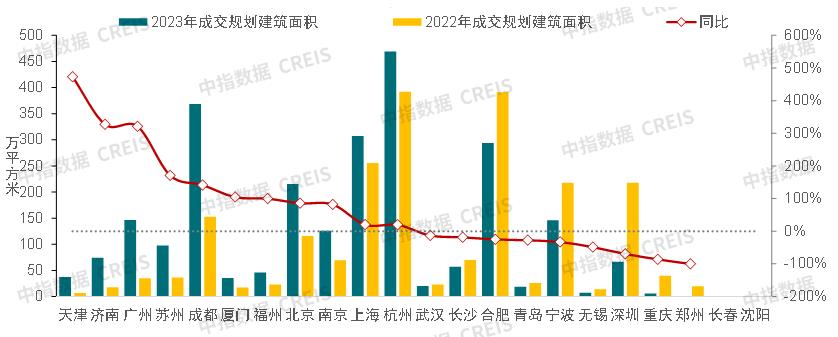

Figure: Comparison of transaction scale of high premium residential land in 22 cities from January to November in 2022 -2023 (city level)

Note: The statistical caliber of plots with high premium rate is that the transaction premium rate is higher than 10%. If the upper limit of premium rate of some plots in Wuhan, Jinan, Hangzhou and Shanghai is lower than 10%, it will also be counted if the transaction hits the top.

Market monitoring: https://www.cih-index.com/

The launch of high-quality land plots has driven the transaction of high-premium land plots in half of the cities to increase year-on-year, and the supply of improved real estate in the future will increase or form some support for the new housing market. In the current market environment, most of the plots that can cause real estate enterprises to actively bid and make high-premium transactions are high-quality plots in the core area. According to the monitoring of the middle finger, from January to November 2023, the transaction scale of high-premium plots in 22 cities was 25.38 million square meters, an increase of 18.7% year-on-year. In terms of specific cities, under the influence of the low base of Tianjin, Jinan, Guangzhou, Suzhou, Xiamen and Fuzhou, the transaction scale of high premium plots increased by over 100% year-on-year; Chengdu has increased the land supply in the core area this year, and the transaction area of high premium plots has also increased by over 100% year-on-year; In Beijing, Shanghai and Hangzhou, the performance of local auctions is stable, with varying degrees of growth. If the high-quality land sold in 2023 gradually enters the market next year, it is expected to provide some support for the sales of new houses in some cities.

In terms of land acquisition enterprises, according to the statistics of the middle finger, as of the end of November this year, central state-owned enterprises accounted for 50% of the accumulated land acquisition amount for centralized land supply in 22 cities, an increase of 13 percentage points over last year; Local state-owned assets accounted for 23%, down 19 percentage points from last year; Private enterprises accounted for just over 20%, an increase of 6 percentage points over last year.

Since the beginning of this year, the proportion of land acquisition by central state-owned enterprises has increased significantly, and local state-owned assets have been weak. On the one hand, in 2023, local governments were under great financial pressure, which was superimposed by the fact that in October last year, "the Ministry of Finance prohibited borrowing to reserve land, and it was not allowed to falsely increase land transfer income through state-owned enterprises, and it was not allowed to falsely increase fiscal revenue under various pretexts to make up for the fiscal revenue gap", and the phenomenon of land acquisition by local platforms was reduced. On the other hand, during the market downturn, the capital advantages of central state-owned enterprises are prominent, especially in hot cities such as Beijing and Shanghai, and the amount of land acquired by central state-owned enterprises is relatively high; Suzhou, Qingdao and Wuhan all increased by more than 20 percentage points compared with last year.

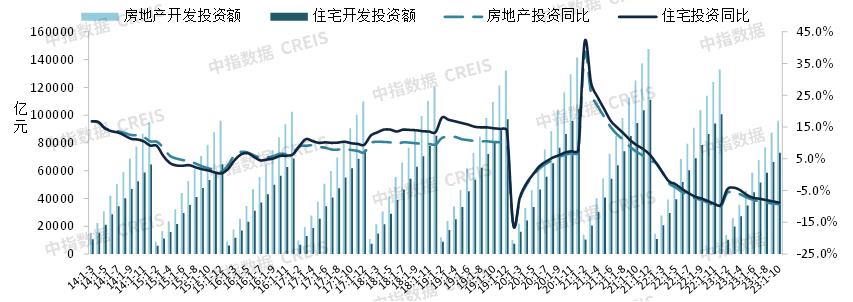

From January to October, the investment in real estate development decreased by 9.3% year-on-year, and the decline continued to expand.

Figure: Cumulative investment in real estate and residential development since 2014 and its year-on-year growth rate.

Source: National Bureau of Statistics,

Middle finger data CREIS (click to view)

The national investment in real estate development has been continuously decreasing since April 2022, and the overall decline has been expanding since 2023.From January to October 2023, the national investment in real estate development was 9.6 trillion yuan, down 9.3% year-on-year. In a single month, the year-on-year decline in investment at the beginning of the year has narrowed compared with the end of last year. However, with the market weakening again, the year-on-year decline in development investment has expanded again, with the year-on-year decline exceeding 10% since May.

Since 2023, the funds in place of housing enterprises have continued to decline year-on-year, and all sources of funds have decreased year-on-year from January to October.From January to October, 2023, the capital in place of real estate development enterprises was 10.7 trillion yuan, down 13.8% year-on-year. Among them, domestic loans were 1.3 trillion yuan, down 11.0% year-on-year; Self-raised funds were 3.5 trillion yuan, a year-on-year decrease of 21.4%; Deposits and advance receipts were 3.7 trillion yuan, down 10.4% year-on-year; Personal mortgage loans amounted to 1.9 trillion yuan, a year-on-year decrease of 7.6%.

Trend Prospect of China Real Estate Market in 2024

Macro-environment: In 2024, the economic growth rate may slow down, and the cross-cycle and counter-cycle adjustment policies are expected to make further efforts.

In the first three quarters of 2023, China’s GDP grew by 5.2% year-on-year, and it is expected that the growth target of around 5% for the whole year can be achieved smoothly. However, in the "troika", the year-on-year growth rate of exports has continued to narrow in recent months, and it has maintained a downward trend in a single month. The year-on-year growth rate of investment in fixed assets has also narrowed to 2.9%, and the decline in investment in real estate development is still expanding. Looking forward to 2024, the global economic growth will slow down, and the external demand may continue to be sluggish. The driving role of the "Belt and Road" in China’s exports is expected to continue to appear, while the scar effect brought by the epidemic is still there. The probability of stronger consumption than expected is low, and the need for stable investment is even stronger. At the end of October 2023, the Central Financial Work Conference proposed to "always maintain the stability of monetary policy, pay more attention to cross-cyclical and countercyclical adjustment, and enrich the monetary policy toolbox". It is expected that monetary policy will further stabilize the economy in the future, and fiscal policy is also expected to cooperate with each other to better release the potential of economic development.

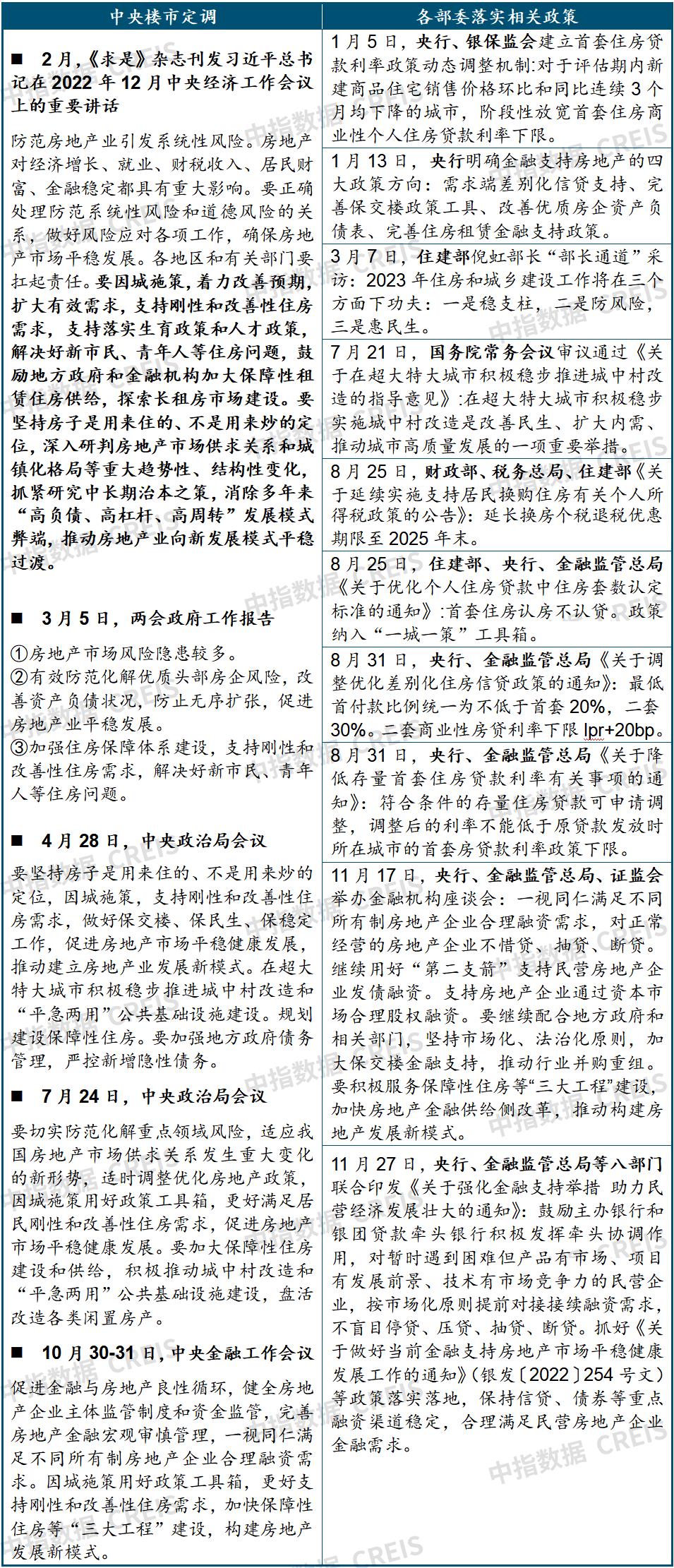

Policy environment: With the adjustment of "major changes in the relationship between supply and demand", it is expected that all localities will continue to optimize the property market policy, and the supporting measures for the "three major projects" are expected to accelerate.

On July 24th, Politburo meeting of the Chinese Communist Party proposed "adapting to the new situation that the relationship between supply and demand in China’s real estate market has undergone major changes", which set the tone for the real estate market. Since then, many ministries and commissions have made clear the optimization direction of real estate policies, and local policies have continued to land. According to the middle finger monitoring, as of November this year, 200 Yu Sheng cities (counties) have issued real estate control policies for over 600 times, and most cities have completely liberalized their restrictive policies.

Table: Policy keynote of the property market in 2023 and relevant policies implemented by various ministries and commissions

Source: Comprehensive arrangement of the Central Finger Research Institute.

At the central level,

In February 2023, Qiushi magazine published the article "Several Major Issues in Current Economic Work" by the Supreme Leader General Secretary, emphasizing the important position of the real estate industry in the national economy, and proposed "to deeply study the major trends and structural changes such as the supply and demand relationship in the real estate market and the urbanization pattern, and pay close attention to studying the long-term and long-term solutions". The government work reports of the two sessions also emphasize "effectively preventing and resolving the risks of high-quality head housing enterprises", "strengthening the construction of housing security system" and "supporting rigid and improved housing demand". In April, it was held in Politburo meeting of the Chinese Communist Party to analyze and study the current economic situation and economic work. The key words of real estate, such as "staying in a house without speculation", "making policy for the city", "supporting rigid and improved housing demand", "guaranteeing the delivery of buildings" and "new development model of real estate industry" all continued the previous formulation, and the overall real estate policy environment remained relaxed.

In July, Politburo meeting of the Chinese Communist Party set the tone for real estate. On the one hand, it clearly stated that "the relationship between supply and demand in China’s real estate market has undergone major changes"; on the other hand, it further clearly promoted the transformation of villages in cities, the "flat and emergency dual-use" public infrastructure and the planning and construction of affordable housing. In this context, the regulatory policies introduced in the past in the short supply stage need to be adjusted and optimized in a timely manner, which opens up space for the regulatory authorities and local governments to optimize the property market policy. Since the end of August, many ministries and commissions have actively expressed their views and introduced specific measures, and restrictive policies in various places have gradually relaxed, and the real estate industry has really ushered in the bottom of policies.

On October 30-31, the Central Financial Work Conference made it clear that "the virtuous circle between finance and real estate should be promoted, the main supervision system and fund supervision of real estate enterprises should be improved, the macro-prudential management of real estate finance should be improved, and the reasonable financing needs of real estate enterprises with different ownership systems should be met equally. Make good use of the policy toolbox because of the city’s policy, better support the demand for rigid and improved housing, and speed up affordable housing ‘ Three major projects ’ Construction, build a new model of real estate development. "

Figure: Frequency of local policies since 2022

Table: Comparison of frequency of major policy types since 2023

Note: A policy in the total column may cover multiple dimensions.

Source: Comprehensive arrangement of the Central Finger Research Institute.

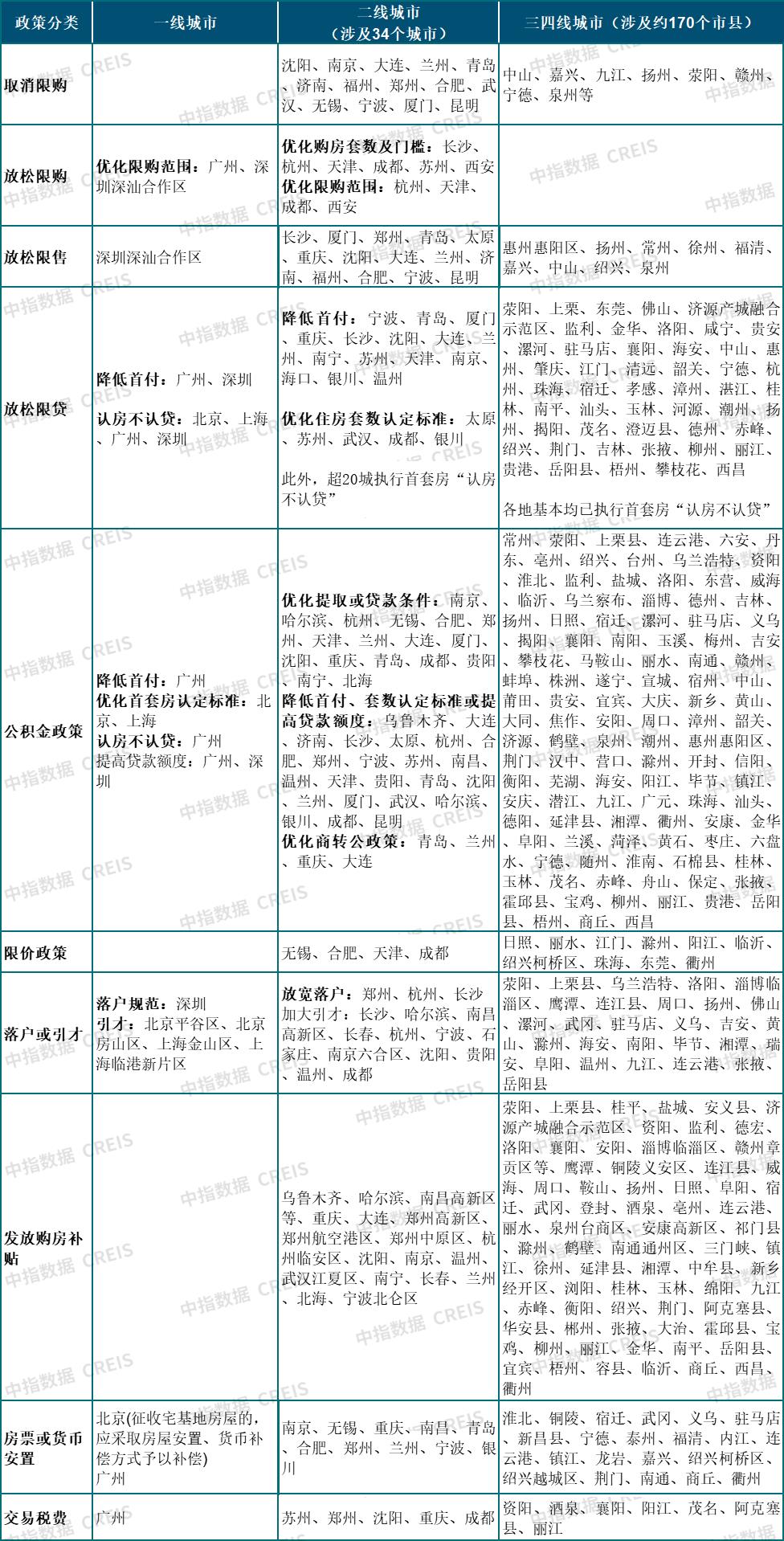

At the local level, since the end of August, various localities have frequently introduced favorable policies, and the first suite in Guangzhou, Guangzhou and Shenzhen has been implemented, and the frequency of policies in September reached the highest level in a single month since the fourth quarter of last year. In terms of purchase restriction, 14 second-tier cities such as Nanjing, Hefei, Jinan and Qingdao completely canceled the purchase restriction policy, and several other second-tier cities relaxed the purchase restriction by optimizing the number of purchase sets, optimizing the scope of purchase restriction and relaxing the restrictions on purchase. Among the first-tier cities, Guangzhou relaxed the purchase restriction in the suburbs.

In terms of loan restriction, all localities have actively implemented differentiated housing credit policies. Most cities have implemented the down payment ratio of 20% for the first set and 30% for the second set of commercial loans, and adjusted the lower limit of the interest rate of the second home loan to LPR+20BP. Some core second-tier cities such as Hangzhou have reduced the down payment ratio to 25% for the first set and 35% for the second set. Among the first-tier cities, the down payment ratio of commercial loans in Guangzhou and Shenzhen has dropped to 30% for the first set and 40% for the second set. In addition, most cities in the country have implemented the policy of "recognizing the house but not the loan" for the first suite.

According to the monitoring of the middle finger, nearly 30 cities have reduced or cancelled the requirement of restricted sales years since 2023; More than ten cities such as Shenzhen, Chengdu and Hefei have optimized the price limit policy; At the same time, more than 30 cities across the country have clearly implemented room ticket placement, and Guangzhou is the first-tier city.

Clearly put forward to explore the policy mechanism of housing ticket placement.

Table: Summary of local real estate easing policies in 2023 (incomplete statistics)

Source: Comprehensive arrangement of the Central Finger Research Institute.

At the same time, the support of various localities has been continuously strengthened. For example, Zhengzhou supports the reconstruction of non-residential rental housing, pointing out that after the expiration of the operating period of rental housing, projects that meet the relevant standards can change the nature of land and be sold as ordinary houses; Wuhan issued a notice stressing the need to revitalize enterprise assets, speed up the revitalization of existing land, and clarify that the government can organize land recovery, planning optimization and re-supply of existing land that has been sold but not yet built. In addition, some cities have accelerated the implementation of the central government’s deployment, and the policy of urban village reconstruction has also been continuously implemented. In October, Guangzhou deliberated and passed the Special Plan for Urban Renewal in Guangzhou (2021-2035) and the Special Plan for Reconstruction of Villages in Guangzhou (2021-2035). In November, the Regulations on Reconstruction of Villages in Guangzhou (Revised Draft for Comment) was publicly solicited for opinions from all walks of life, providing guarantee for accelerating the reconstruction of villages in cities.

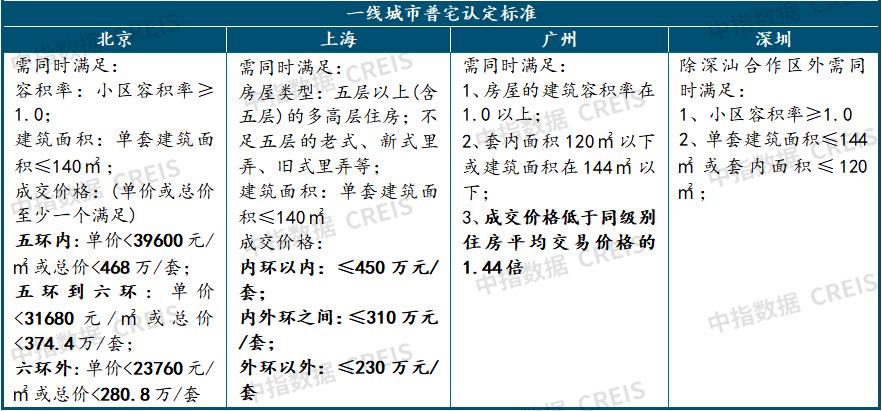

In addition to the above policy measures, some cities have also improved their policy toolboxes from the aspects of optimizing the identification standard of ordinary houses (for example, Shenzhen cancelled the requirement that the actual transaction price is less than 7.5 million yuan in November), optimizing the supervision of pre-sale funds, increasing the subsidy for house purchase, reducing the intermediary rate, and reducing the exemption period of value-added tax, so as to promote the release of rigid and improved housing demand.

On the whole, the continuous downturn of the real estate market and the accumulation of industry risks have brought adverse effects on the stability of the whole macro-economy and financial system, and stabilizing the real estate market is very important for stabilizing the macro-economy market. Under the important background that Politburo meeting of the Chinese Communist Party proposed to "adapt to the new situation of great changes in the supply and demand relationship of China’s real estate market", the restrictive policies introduced in the overheated market in the past are gradually withdrawing or optimizing.

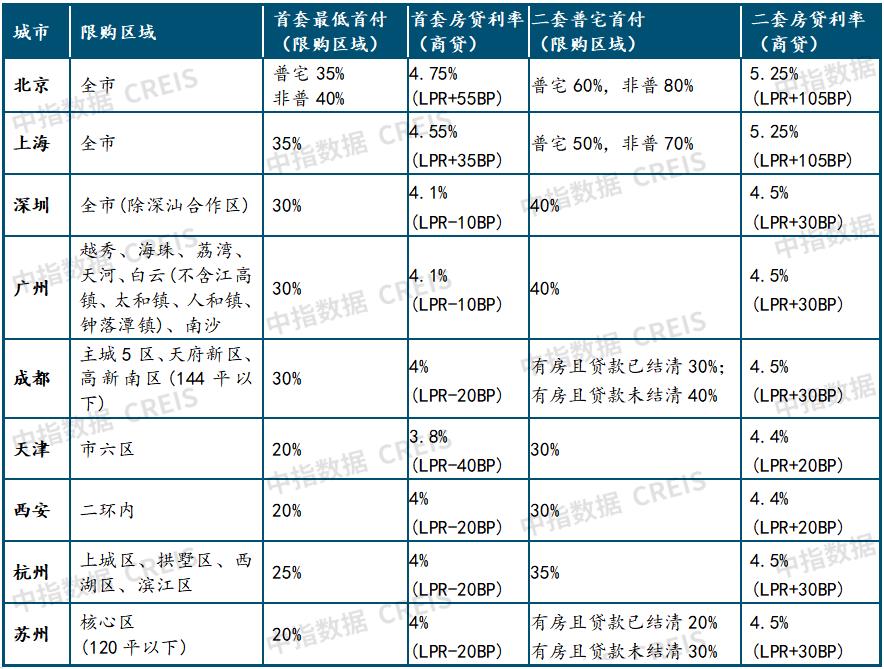

Table: Current situation of purchase restriction and loan restriction policies in core first-and second-tier cities (as of November)

Source: Comprehensive arrangement of the Central Finger Research Institute.

From the perspective of policy trends, on the demand side, reducing the cost of buying houses and lowering the threshold for buying houses are still the focus of policy optimization. In the future, the policies of first-tier cities may continue to be optimized. Beijing and Shanghai are expected to reduce the down payment ratio of second homes, lower the mortgage interest rate, optimize the standard for identifying ordinary houses, and reduce transaction taxes and fees. In addition, it is also possible for first-tier cities to optimize suburban purchase restrictions according to regional policies; Core second-tier cities are expected to further relax the purchase restriction policy, and it is expected that more cities will completely cancel the purchase restriction; More low-level cities may promote the release of housing demand by issuing housing subsidies.

On the enterprise side, the policy will still focus on alleviating the financial pressure of real estate enterprises and preventing and controlling risks. Financial institutions may continue to increase financial support for housing enterprises and implement detailed policies, and the financing environment of enterprises is expected to improve. In addition, the "Baojiaolou" funds and supporting measures may be further followed up to stabilize market expectations. At the same time, the policy of revitalizing the stock of houses for sale, non-residential idle projects and undeveloped land is also an important aspect of providing liquidity support for enterprises.

In addition, the supporting measures for the construction of the "three major projects" are expected to be further accelerated. It is expected that the regulatory authorities will further clarify the relevant rules for the transformation of urban villages, and more cities will implement the supporting policies for the transformation of urban villages. Promoting the construction of "three major projects" will play an important role in stabilizing investment next year, and will also play a positive role in restoring sales and stabilizing expectations.

Under the neutral hypothesis, the sales area of commercial housing in China will decrease by about 5% in 2024. If the renovation of villages in cities is accelerated, sales are expected to increase slightly. The downward trend of construction and investment is difficult to change.

According to the "dynamic model of the medium and long-term development of China real estate industry", combined with the predictions of domestic and foreign economic research institutions on the economic environment in 2024, and referring to recent macro policies and the spirit of important conferences, the following assumptions are put forward for the real estate market in 2024:

Hypothesis 1: The macro-economy is gradually recovering, and the GDP growth rate is slower than that in 2023 (GDP growth is between 4.5% and 5.0%);

Assumption 2: Monetary and credit policies continue to exert efforts to stabilize the economy, with a year-on-year increase of about 9.5% in M2;

Hypothesis 3: the real estate control policy continues to be loose, because the city’s policy is still strong;

Hypothesis 4: Policies such as the transformation of villages in cities have been substantially implemented.

Under the premise of meeting the hypothetical conditions and not exceeding the expected events, according to the "China real estate industry long-term development dynamic model", the national real estate market will present in 2024.

"There is still downward pressure on the sales scale, and the newly started area and development investment may continue to fall".

Table: Forecast Results of National Real Estate Market Indicators in 2024

Source of data: calculation by the Central Finger Research Institute.

On the demand side, looking forward to 2024, the recovery of the real estate market still depends on whether the buyers can expect to repair it. According to the "Medium-and Long-term Development Dynamic Model of China Real Estate Industry", under neutral circumstances, the sales area of commercial housing nationwide will decrease by 4.9% year-on-year in 2024, with a scale of about 1.1 billion square meters. Under optimistic circumstances, in 2024, the macro-economy will continue to recover, residents’ willingness to buy homes will improve, and the reconstruction of superimposed villages in the city will advance as scheduled, and the sales area of commercial housing in the country may increase slightly, with an absolute scale slightly higher than 1.2 billion square meters; It is worth noting that 2024 is the start year of the renovation of villages in megacities. The actual pull of the renovation of villages in cities on housing demand is limited, but it is very important to the expected impact. Under pessimistic circumstances, in 2024, under the influence of the downward pressure of macro-economy, the unstable income expectation of residents and the continuous decline of house prices, the sales area of commercial housing in China decreased by about 8.6%, and the scale was less than 1.1 billion square meters.

In addition, the scale of the new housing market is estimated from the land transaction scale in the past two years. According to the data of the middle finger, the total planned construction area of residential land and commercial land transactions nationwide is 1.67 billion square meters in 2022, and 910 million square meters in January-November 2023. It is optimistic that half of the land transactions in the past two years will enter the market in 2024, and the supply scale of the new housing market is expected to be around 1.3 billion square meters, which will also provide some support for the sales market to achieve 1.2 billion square meters in optimistic circumstances.

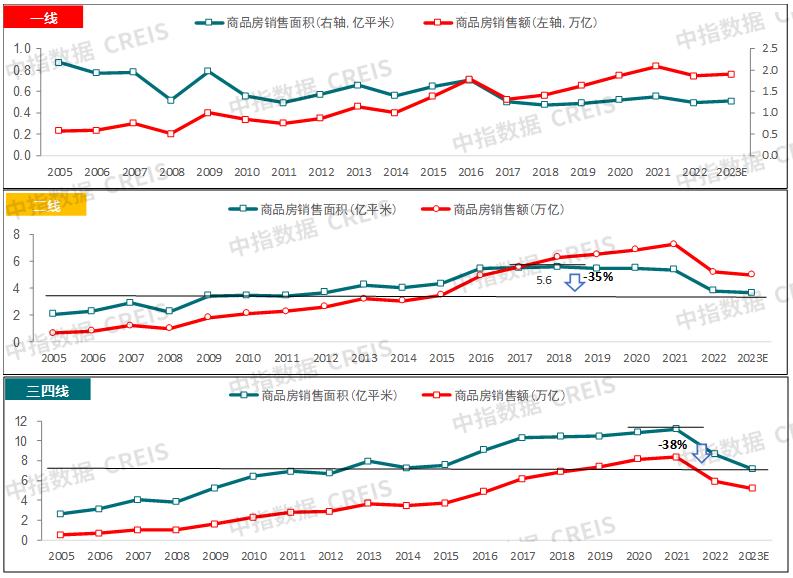

Figure: Changes in the sales area and sales volume of commercial housing in cities since 2005.

Source: National Bureau of Statistics, local statistical offices,

Middle finger data CREIS (click to view)

In terms of cities, the sales area of new houses in first-tier cities may continue to grow slightly. In 2024, there is still much room for optimization in policies such as restricting purchases and loans in first-tier cities, and the process of urban village reconstruction is expected to accelerate. The increase in quality supply is also expected to support the market. It is expected that the sales area of new houses in first-tier cities will continue to increase steadily.

The market in second-tier cities is expected to stabilize at the bottom in 2024. In the past two years, the sales area of commercial housing in second-tier cities has dropped significantly. Compared with history, the sales scale in 2023 has dropped by about 35% compared with the high point in 2018, and has fallen back to the level in 2012, which is basically the same as that in 2022. The bottom of new house sales has gradually stabilized. Looking forward to 2024, the short-term inventories of cities such as Hangzhou, Chengdu and Xi ‘an are relatively reasonable. With the continuous optimization and adjustment of the policy side, the sales scale of new houses is expected to remain at a high level; Nanchang, Wuhan, Zhengzhou and other cities have limited space for policy optimization, and inventory destocking is under pressure. It may still take time for the short-term market to get out of the bottom; Fuzhou, Tianjin and other cities have great pressure to destock, and the market adjustment situation is short-term or difficult to change. In addition, with the gradual adjustment of market volume and price in place, the demand of cities with oversold market in recent two years is expected to be repaired.

The scale of new home sales in third-and fourth-tier cities is expected to continue to decline in 2024. In 2023, the sales area of commercial housing in third-and fourth-tier cities continued to decline year-on-year, which was 38% lower than the historical high point in 2021. The market adjustment was greater than that in first-and second-tier cities, and the sales scale had dropped to the level of 2014-2015. At present, the market sentiment in third-and fourth-tier cities is relatively low, and the overdraft of demand, falling house prices, and insufficient policy-driven effects are important reasons. In 2024, the incremental policies in third-and fourth-tier cities are limited as a whole, and some cities may promote the release of demand by issuing housing subsidies, but the effect may be weak. At the same time, the per capita housing area in many third-and fourth-tier cities is large, and the scale and space of the new housing market in the future are limited as a whole. On the whole, housing in third-and fourth-tier cities is gradually returning to the consumption attribute, and the future housing demand depends more on factors such as rural population entering cities and residents’ purchasing power. In 2024, the performance of various influencing factors may be difficult to improve significantly, and it is expected that the sales scale of new houses will continue to decline.

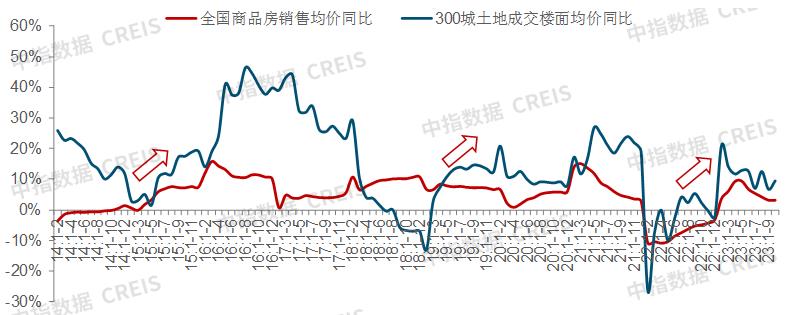

Figure: Since 2014, the average sales price of commercial housing in China and the average floor price of land (residential+commercial office) in 300 cities have accumulated year-on-year.

Market monitoring: https://www.cih-index.com/

In terms of price, from the trend of housing prices, the listing volume of short-term second-hand houses may still be at a high level, and the price decline trend is expected to continue under the weak demand, and the price of second-hand houses will fall, which may lead to more demand for buying houses being transferred to the second-hand housing market. In order to speed up the withdrawal of funds, the price reduction promotion of new housing projects will continue to increase, and the overall performance of new housing prices is expected to be weak.

From the structural point of view, on the one hand, since 2023, the average floor price of land transactions in 300 cities nationwide has increased by about 10% year-on-year. The increase in the volume of high-quality plots has led to a structural increase in the average floor price of transactions, and this part of the plots has gradually entered the market, which is expected to have a structural drive on the sales price of new houses. On the other hand, in 2024, the real estate market in first-and second-tier cities is expected to maintain a certain degree of activity, and the market share is expected to continue the upward trend in 2023, thus further driving the structural increase of the national average sales price. According to the model calculation, under neutral circumstances, the average sales price of commercial housing in China will increase by about 2.6% year-on-year.

Based on a comprehensive analysis of the trend of commercial housing sales area and average selling price, it is estimated that the national commodity sales will decrease slightly by 2.4% in 2024. Under optimistic circumstances, in 2024, the national sales of commercial housing will increase slightly year-on-year, with an increase of about 4%.

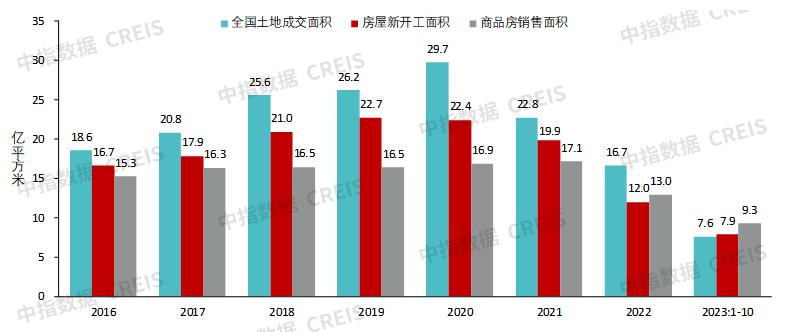

Figure: Newly started housing area, commercial housing sales area and national land transaction planning construction area since 2016.

Source: National Bureau of Statistics,

Middle finger data CREIS (click to view)

On the supply side, the scale of new construction of housing enterprises is still restricted by the slow pace of new house sales recovery, land shrinkage and high existing stock. It is difficult to change the downward trend of new construction in 2024. According to the model calculation, under neutral circumstances, the new construction area in 2024 will drop by about 10% year-on-year, and the absolute scale will drop to 830 million square meters. It is worth noting that 2024 is the first year of accelerating the transformation of villages in cities, and the overall scale of new construction is relatively small. Under optimistic circumstances, the new construction area decreased slightly by 2.7% year-on-year, and the scale dropped to about 900 million square meters.

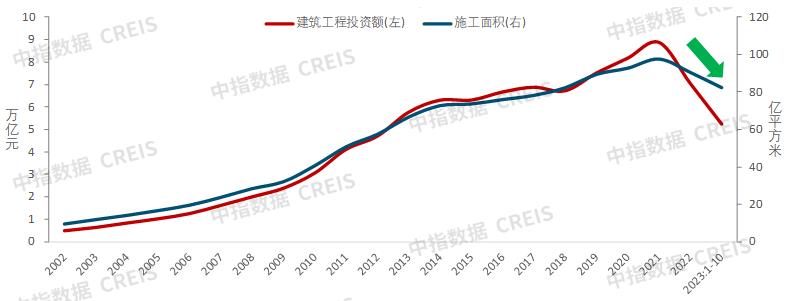

Figure: Comparison of investment in construction projects and building construction area since 2002.

In terms of investment, on the one hand, factors such as the decline in new construction and the peak construction will continue to restrict the investment restoration of construction projects, and the shrinking trend of land transactions has not changed in the past two years, or the land purchase fee has further declined. On the other hand, the policy of "guaranteeing the delivery of buildings" and the improvement of buyers’ preference for existing houses are expected to continue to support the completion, which in turn will play a driving role in real estate investment. Under neutral circumstances, the investment in real estate development decreased by about 6% year-on-year in 2024. Under optimistic circumstances, the renovation of villages in cities and the construction of affordable housing will exert their strength, and the investment in real estate development will be basically the same as that in 2023.

Suggestions on business strategy of housing enterprises in 2024

In terms of sales, according to the data of the middle finger, from January to November 2023, the total sales of TOP100 real estate enterprises was 5,737.90 billion yuan, down 14.7% year-on-year, and the decline was 1.6 percentage points higher than that of the previous month. The sales of housing enterprises in all camps decreased year-on-year. The sales of TOP10 housing enterprises decreased by 9.3% on average, while the sales of TOP11-30, TOP31-50 and TOP51-100 housing enterprises decreased by 14.6%, 17.7% and 25.1% respectively.

Figure: Average sales and growth rate of TOP100 real estate enterprises from January to November from 2021 to 2023.

From the perspective of enterprise types, central state-owned enterprises have achieved growth. Among TOP50 enterprises, the sales of central state-owned enterprises increased by 8.2% on average, while the sales of steady private enterprises decreased by 6.8% on average, mixed-ownership enterprises decreased by 15.3%, and private enterprises in danger decreased by 48.0%.

In terms of land acquisition, from January to November 2023, the total land acquisition of TOP100 enterprises was 1,085.5 billion yuan, down 6.6% year-on-year, and the decline was 3.4 percentage points lower than that of the previous month. Among them, among the top 50 enterprises and the top 100 enterprises, the number of central enterprises and state-owned enterprises accounted for more than 70%. Head enterprises insist on fixing production by sales and living within their means to maintain investment efficiency and stable operation.

In terms of financing, from January to November 2023, the total bond financing of real estate enterprises was 628.79 billion yuan, down 8.6% year-on-year, and the decline was 0.3 percentage points narrower than that of the previous month. Among them, the real estate industry credit bond financing was 395.95 billion yuan, down 6.8% year-on-year, accounting for 63.0%; The issuance of overseas bonds was 18.38 billion yuan, a year-on-year increase of 4.4%, accounting for 2.9%; ABS financing was 214.46 billion yuan, down 12.6% year-on-year, accounting for 34.1%.

Judging from the debt balance, as of the end of October, the balance of bonds due in 2023 was 116.53 billion yuan, of which overseas bonds accounted for 23.4% and credit bonds accounted for 76.6%. The balance of bonds due in 2024 was 787.34 billion yuan, of which overseas bonds accounted for 34.0% and credit bonds accounted for 66.0%, and the overall debt repayment pressure remained.

In 2023, China’s real estate market is still in the downward stage, and the pressure on housing enterprises’ funds has not changed. Under the new situation of great changes in supply and demand, the market structure and enterprise structure continue to face adjustment. In the long run, the scale of the real estate market is still 10 trillion, and there are still structural opportunities in different cities and different needs. At the same time, the direction for the industry to explore new development models has gradually become clear. Housing enterprises should seize market opportunities and take the initiative to adapt to the new situation and achieve high-quality development. Looking forward to 2024, the national new housing market is still facing downward pressure in the short term, and different housing enterprises need to formulate corresponding strategies according to their own conditions and cross the cycle.

In view of the real estate enterprises in danger, it is suggested to take active actions to solve the current problems.

On the one hand, with the help of the current financial policy window, actively connect with financial institutions, fully display the debt, at the same time, actively market the payment back and make every effort to ensure delivery; On the other hand, we should dispose of assets, speed up clearing, seize policy opportunities to revitalize the stock, including unsold houses, non-residential houses, and undeveloped land, and take the initiative to seek opportunities to revitalize related assets by converting them into rented houses or affordable houses, and bear corresponding losses for clearing.

For stable housing enterprises, seize market opportunities to actively market, quickly withdraw funds, and explore new development models at the same time.

First, actively market quick payment. At present, the scale of the real estate market is still there, and the policy environment will remain relaxed in the medium and long term. The policies of core first-and second-tier cities have room for further optimization, so enterprises should seize the market window and actively market. At the same time, actively cooperate with financial institutions to broaden financing channels and reduce financing costs.

Second, optimize the urban layout structure, focus on the core cities, and maintain a certain scale of land acquisition. Land is an important means of production for housing enterprises, and enterprises must maintain a certain scale of land acquisition in order to achieve sustainable development. At present, the market is still in a period of adjustment, and precision investment is still the most important investment strategy. Housing enterprises still need to choose the best in land acquisition, focus on the core areas of core cities, and ensure the safety of projects. In addition, the renovation of villages in cities will receive more policy and financial support next year, and housing enterprises should actively seek opportunities to participate in the renovation of villages in cities.

Third, polish the product strength and grasp the mainstream demand. Good products and good services in the future are the key for housing enterprises to stand on the market. Under the trend of commodity housing returning to commodity attributes, consumers will have higher requirements for product quality and service quality of housing enterprises in the future, and good products and services will have stronger market competitiveness; At the same time, the improved demand has a large development space in the future, and only by grasping the mainstream demand can we better promote the return of sales funds.

Fourth, attach importance to both light and heavy, and actively explore new development models. Under the new situation, with the industry exploring new development models, real estate enterprises should also take advantage of the situation and actively explore new models suitable for their own development, with emphasis or important direction, and there is room for development in agent construction, property services, commercial operation and long-term rental apartments. For example, in the field of agent construction, in recent years, the local state-owned land acquisition rate is low, the construction of local affordable housing is accelerating, the agent construction market is still in a period of rapid development, and there is still much room for improvement in the penetration rate and scale of the agent construction industry.